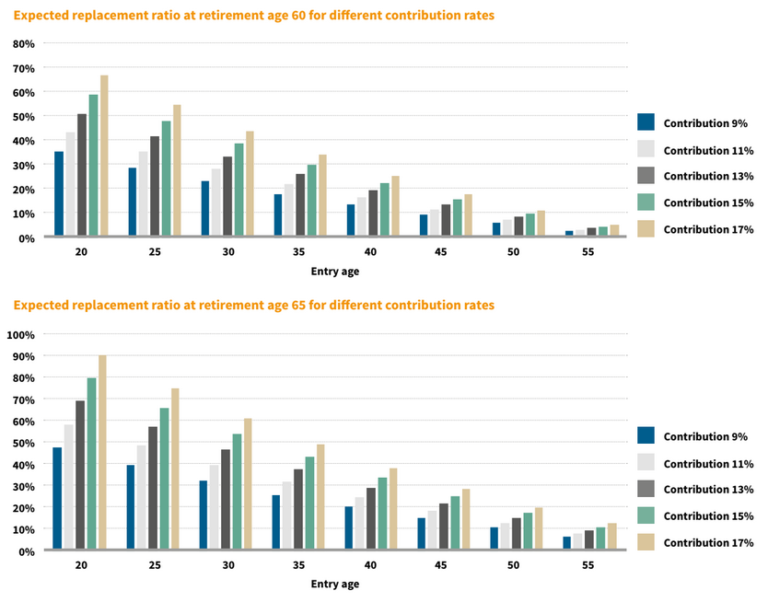

Working South Africans require meaningful connections to make better financial decisions, as they are projected to retire on only 40% of their final salary, according to financial services company, Alexander Forbes.

Working South Africans require meaningful connections to make better financial decisions, as they are projected to retire on only 40% of their final salary, according to financial services company, Alexander Forbes.

Current retirees’ starting pensions amounted to 31% in 2020, an improvement from the previous year’s 28%. This is still a long way off from what is considered ideal, said John Anderson, executive, Investments, Products and Enablement, Alexander Forbes

“They need better connections to their retirement funds, to their options at key stages in their careers and to the long-term impact of their decisions to change their retirement picture for the better. In addition, planned reforms by National Treasury to introduce the “two-bucket system” will help improve the outcomes further.”

The main driving forces resulting in the current disconnect include:

- A one-dimensional employee benefit consulting framework that does not consider the employer, fund or individual holistically.

- One-size-fits-all approaches being used in designing employee benefit programmes.

- Ineffective communication strategies.

- High levels of indebtedness among members.

- The impact of Covid-19, which amplified existing risks and challenges.

- Low levels of financial literacy and engagement among members.

- Gender pay inequality, where females continue to earn less than their male counterparts, which translates into lower contributions for females.

Using empirical data sourced from almost a million members of retirement funds, Alexander Forbes Member Insights exposes, explores and extrapolates trends in fund member data to create insights that can be used to improve outcomes.

The report is based on members showing an average age of 40, with single members earning an average of R19,327, and an average household income of R28,635.

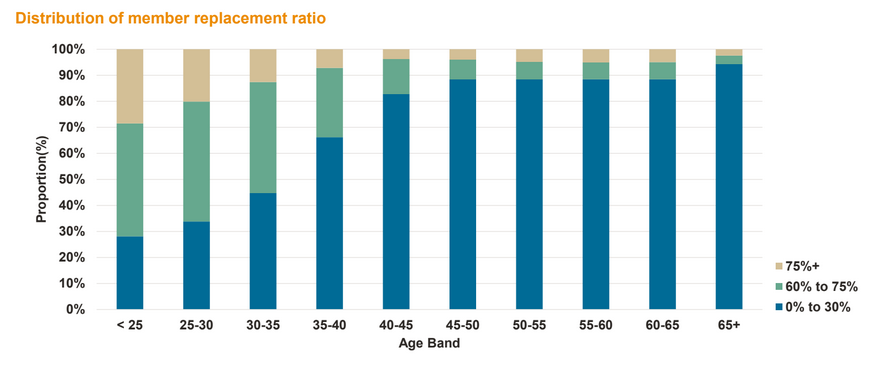

Only 6 in every 100 members can retire on more than 75% of their pensionable salary, said Ntsheki Molefe, regional executive, Retirements, Alexander Forbes.

According to Member Insights, only about 6% of retirement fund members can expect an income in retirement above 75% of their pensionable salaries. However, retirement funding stakeholders, including employers, trustees and advisers, can improve this by forming more meaningful connections with members.

“This year, data beyond the traditional retirement data was linked to provide more thorough insight. The results of Member Insights serve to amplify our collective responsibility to better connect with members via access to information, education, counselling and advice. We have hard evidence of the impact on decisions when such connections are improved and are convinced that this will make a positive impact on people’s lives,” said Anderson.

Covid-19

The implications of Covid-19 on retirement outcomes are evident in the research, which found that:

- About 30% of retirement funds implemented contribution holidays or reduced contributions.

- Many of the funds had since recovered and only 5% of funds still have these relief measures in place.

- Average contribution rates reduced slightly from 14.18% to 14.10%.

Reforms to address lack of savings

Alexander Forbes said it supports proposed reforms to address the lack of savings in South Africa in a two-bucket proposal that will allow for greater preservation with limited pre-retirement withdrawals from retirement.

Approximately 90% of members do not preserve when changing employers, largely as a result of a lack of financial literacy or the need for immediate access to cashflow.

Alexander Forbes said it has evidence of substantial increases in preservation when the appropriate engagement mechanisms are introduced through the employer and fund to enable better connections with members.

The two-bucket proposal provides an additional pragmatic response to meet both the short-term and long-term needs of members. Further details are expected to be tabled with the Medium Term Budget Policy Statement on 4 November 2021.

“It is important for members to have full access to professionalised retirement benefit counselling and for the two-bucket solution to balance the trade-offs between long-term retirement savings goals and short-term financial needs,” said Molefe.

Millennials have been hardest hit financially by Covid-19 and are at the highest risk of loan defaults. The analysis found that at least 14.11% of loans taken by Early Millennials were in default, followed by Late Millennials at 4.79%, Generation X at 2.27% and Baby Boomers at just 0.94%.