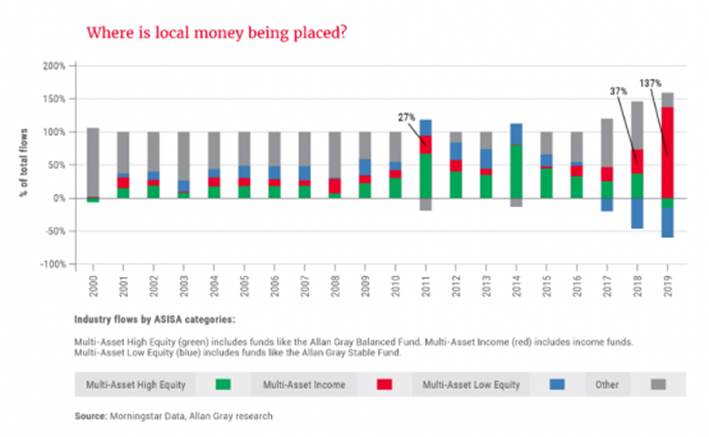

Over the last two years South African investors have moved a huge amount of money into income funds. As the graph below from Allan Gray shows, 2018 and 2019 saw the biggest inflows into this category in 20 years.

At the same time, money has been moving out of local balanced funds.

This suggests that many investors are worried about having any exposure to the South African stock market. They are instead moving to the perceived safety of cash and bonds.

This is despite the fact that 2017 and 2019 were both good years on the JSE. The market was up 21% in 2017, and 12% last year. This performance was however split by the poor -8.5% return in 2018.

As a result, the FTSE/JSE All Share Index has shown an annualised gain of just 7.4% per annum over the past three years. This is around half of its historical average, and below the returns of around 8-10% per annum currently available from many local multi-asset income funds.

Sense and sensibility

Investor concerns about this weak stock market performance have also been compounded by the state of the local economy. South Africa’s low growth, and the slow pace of reforms to correct it, have led many to decide that the prospects for local stocks are poor.

The decision to move away from the JSE may thereforeseem entirely reasonable. However, anyone investing for the long term needs to consider whether recent history is really a reliable indicator of what they can expect in the future.

As Beatri Faul, investment specialist at Allan Gray, points out, investors shouldn’t be too quick to equate a country’s economic prospects with the outlook for its stock market.

“A strong, growing economy does not necessarily mean that you are guaranteed strong performance from all companies on the stock market,” Faul notes. “This is because a strong economy likely introduces competition, which brings down the prices these companies can charge, and subsequently profits.”

Similarly, a poor economy does not necessarily mean that equity returns will be unattractive.

“In a slower growing economy there is less competition, and while there is also less money to spend, goods and services are still needed, therefore there is still opportunity for some companies to thrive,” Faul points out.

It is even the case that the strongest companies can perform really well in a difficult environment as their weaker competitors fail. It may also be possible for them to expand their businesses by buying good assets at cheap prices.

Where we are

Any equity investment also has to take into account how much you are paying for the shares you are getting.

“Price and value are the most important determinants when it comes to investment returns,” Faul notes. “Because the South African stock market has been driven down by negative sentiment over the past few years, you are able to pay reasonable prices for attractive opportunities today. This increases your chances of achieving good performance in the future.”

As Pieter Koekemoer, head of personal investments at Coronation Fund Managers, suggests, investing is about looking forwards, not backwards.

“It’s incredibly easy to construct an investment portfolio that you will feel good about today based on current sentiment, recent past performance and the concerns we see,” Koekemoer says. “What is much harder is to think about how much of how you feel is already in the price.

“How much of the weak returns you’ve seen domestically is justified, given the poor economic environment? And how much is too pessimistic and results in great prices now that will give you great returns over the next five to 10 years?”

It’s not about blind optimism

This doesn’t mean Koekemoer is bullish about the outlook for the South Africa. He thinks it is likely that the economy will continue to struggle.

However, investors who are moving out of stocks and into income funds need to bear two things in mind. The first is that they are not necessarily avoiding risk.

As Koekemoer points out: “The income assets and shares are issued by the same businesses, participating in the same economy.”

The increased demand for income assets also means that a larger pool of capital is chasing returns in that part of the market. There is, however, not an infinite supply of good quality bonds issued by local companies. The result is that people may be taking more and more credit risk, without realising it.

The second is that it is important to separate sentiment from fundamentals.

“The fact that you know about the economic situation, and are very concerned about it, does that mean you are still going to get very weak returns from local growth assets?” asks Koekemoer. “Of course it is possible, but the probability of a better outcome has increased dramatically just because valuation levels are so attractive.

“Most of SA Inc is now trading on single digit PEs [price-to-earnings multiples] with somewhere between 5% and 10% dividend yields,” he adds.

“Those are super-attractive valuations and you don’t need an economic miracle to do well out of owning those assets. You only need a slightly better environment than the current 0-1% growth per annum over the next decade and then you are going to do quite well.”